This is the beginning of the season when companies that are on a calendar year begin their strategic and long-term planning. Ventana Research performed an extensive investigation in this area with our long-range planning benchmark research. Strategic and long-range planning is a process and discipline that companies use to determine the best strategy for succeeding in the markets they serve and then ensure they have the capabilities and resources needed to support their strategic objectives.

I use the term “strategic planning” to mean the formal conceptualization of strategy, which is more qualitative than quantitative. Typically, it involves a relatively small number of people on the senior leadership team. Long-range planning, on the other hand, is the formal quantification of the strategic plan, which translates ideas into numbers. This process involves fewer and more senior people than the annual budget, and it is designed to serve as a bridge that connects an organization’s strategic conceptualization with its operational planning and financial budgeting.

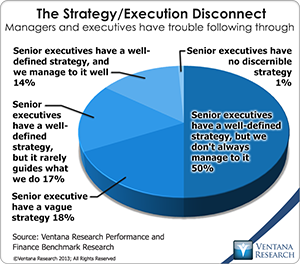

Our research shows that nearly two-thirds (64%) of participants – all  of whom are involved in long-range planning – are satisfied with the results of their process. If that was all there was to it, companies wouldn’t have to worry about how well they connect strategy with execution. However, other financial performance management research we conducted, which includes a broader sample of executives and managers in a variety of corporate roles and departments, paints a different picture. Among those participants, two-thirds (64%) said that their company’s executives have a well-defined strategy, but only 14 percent said that their company manages it well on a consistent basis.

of whom are involved in long-range planning – are satisfied with the results of their process. If that was all there was to it, companies wouldn’t have to worry about how well they connect strategy with execution. However, other financial performance management research we conducted, which includes a broader sample of executives and managers in a variety of corporate roles and departments, paints a different picture. Among those participants, two-thirds (64%) said that their company’s executives have a well-defined strategy, but only 14 percent said that their company manages it well on a consistent basis.

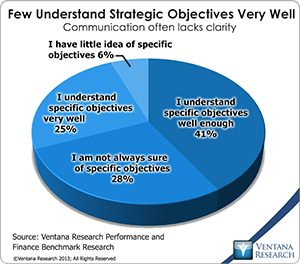

There are complex reasons for the disconnect between corporate strategizing and day-to-day execution. A clear statement of strategic objectives is necessary, of course, but translating it into objectives for business units and individuals is another matter.  Typically, executives use a combination of methods for communicating strategy and goals, including verbal iterations, electronic messages and scorecards with quantitative objectives. Executives may think they are communicating effectively, but often their efforts fall short. Our research finds that only one-fourth of participants understand these objectives well. This is often the case, as our long-range planning research finds that only 27 percent of executives communicate clearly and – just as important – consistently. As well, a common management approach is to set specific, measurable objectives for each business unit: About two in five do that. However, these objectives typically focus mainly on financial measures and do not include the nonfinancial objectives that are critical to achieving corporate strategy, among others market share, quality, customer satisfaction and time to market. Fewer than half (45%) of companies lay out formal, strategy-driven objectives in a scorecard, and almost none of those outside of financial services incorporate risk factors as part of their formal assessments. Only one in five find that when they need to determine the underlying facts behind numbers, it’s easy to determine the “what, why and how” behind them. Nearly half (45%) present little or no information about the company’s operating data, and 80 percent get little or no information about leading indicators that would enable managers to anticipate opportunities or issues.

Typically, executives use a combination of methods for communicating strategy and goals, including verbal iterations, electronic messages and scorecards with quantitative objectives. Executives may think they are communicating effectively, but often their efforts fall short. Our research finds that only one-fourth of participants understand these objectives well. This is often the case, as our long-range planning research finds that only 27 percent of executives communicate clearly and – just as important – consistently. As well, a common management approach is to set specific, measurable objectives for each business unit: About two in five do that. However, these objectives typically focus mainly on financial measures and do not include the nonfinancial objectives that are critical to achieving corporate strategy, among others market share, quality, customer satisfaction and time to market. Fewer than half (45%) of companies lay out formal, strategy-driven objectives in a scorecard, and almost none of those outside of financial services incorporate risk factors as part of their formal assessments. Only one in five find that when they need to determine the underlying facts behind numbers, it’s easy to determine the “what, why and how” behind them. Nearly half (45%) present little or no information about the company’s operating data, and 80 percent get little or no information about leading indicators that would enable managers to anticipate opportunities or issues.

Another aspect of knowing how to manage to the company strategy is understanding how the objectives and actions of one part of the business affect the others. Since most companies do not operate in a rigid command-and-control environment, it is important for managers in one area of the business to be able to anticipate how a change in their part of the company will affect others. An important objective in any corporation is to ensure that strategy and objectives are aligned across departments and business units. Yet only one-fourth of our participants said they have a clear understanding of the specific goals of other parts of the business, such as sales quotas, production targets and profitability, and how these affect their own area. This helps explain other findings described above, such as why so few companies react to changes in their overall business in a well-coordinated fashion – and why it is so common for the left hand not to know what the right is doing.

Since in business the only constant is change, it’s crucial for companies to ensure that they maintain strategic alignment when managing change. Unfortunately, few do. Only 14 percent said that when market or economic conditions change, their company’s response is well coordinated. While six in 10 said their response is somewhat coordinated, I think “somewhat” is an unacceptable standard because it results in diminished performance. After all, a “somewhat coordinated” juggler drops a lot of balls. Improving coordination is an area in which better communication across the company and a clearer view of operations are likely to improve performance in a sustainable fashion. Issues of coordination generally arise from a lack of communication or information availability, both of which reflect what information a company gathers and how it makes it accessible. When the problem is an inability to coordinate actions, the underlying issue usually is an inability to share information easily. Here again, having the means to bring together information from multiple data sources can make it feasible to increase the visibility of actions and status across functional silos.

Improving the connection between strategy and execution starts with a relatively simple conversation between the CEO on the one hand and executives and managers on the other. If asking “What is our strategy?” elicits answers that are inconsistent or rambling (or just blank stares), there’s a strategy communication issue. If the answer to the follow-on question “Can you measure how well you are performing to the company’s strategic objectives?” is no or “sort of,” then the company has a performance measurement or data availability issue or both. Addressing these gaps can go a long way toward diminishing disconnects between strategy and execution. Even if your company does an excellent or very good job of connecting strategy and execution, there is still likely to be room for improvement, especially in terms of providing executives and managers with a more complete view of what’s happening outside of the company, including market trend information and competitive intelligence. Despite a massive, two-decades-long investment in making business data of all types widely available, a majority of companies have yet to fully break free of process and management behavior constraints that are artifacts of a bygone, information-poor era. At the start of the strategic and long-range planning season, it’s time to think about translating all of the thoughtfulness and hard work into better execution.

Regards,

Robert Kugel – SVP Research

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).