An external audit examines an organization’s performance of accounting tasks. It validates the soundness of accounting systems and policies and compliance with generally accepted accounting principles in preparing financial statements – chiefly the income statement, balance sheet and statements of cash flow and equity. The auditor certifies that there are no material errors or omissions, and that the financial statements are compliant with requirements. Technology can transform this process to provide multiple benefits to audit firms and workers, making accounting cool again by using a continuous audit approach.

I recently wrote about the virtual audit, an evolutionary step from the remote audit method that became necessary during the pandemic. It’s an approach where auditors take full advantage of advanced software to .png?width=300&height=300&name=Ventana_Research_2023_Assertion_DigiFin_Virtual_Audit_Adoption_26_S%20(1).png) achieve dependably higher audit quality with less effort. The virtual audit structure also enables audit firms to adopt a continuous audit where tests and tasks are spread out over a fiscal year to better balance the need for resources, avoiding period-end spikes and enabling audit firms to support a larger list of clients than with conventional auditing methods. Audit firms are already doing this to some extent, but remote access broadens the scope of how testing and review calendars are structured to better balance workloads over a year. Ventana Research asserts that by 2026, more than one-half of organizations will adopt some form of a virtual audit.

achieve dependably higher audit quality with less effort. The virtual audit structure also enables audit firms to adopt a continuous audit where tests and tasks are spread out over a fiscal year to better balance the need for resources, avoiding period-end spikes and enabling audit firms to support a larger list of clients than with conventional auditing methods. Audit firms are already doing this to some extent, but remote access broadens the scope of how testing and review calendars are structured to better balance workloads over a year. Ventana Research asserts that by 2026, more than one-half of organizations will adopt some form of a virtual audit.

A virtual audit differs from the remote version by providing the audit firm’s team with remote access to all necessary systems, such as general ledgers, the consolidation application and close management software. This can substantially reduce and perhaps all but eliminate the “provided by client” element of an audit – a request by the auditor for information and supporting documents – because the process of gathering the information is mostly self-service. Because the auditor can access systems directly, this approach saves time on both sides of the process, especially in the inevitable back and forth emails for clarifications and follow-ups.

Giving auditors read-only access to files provides a layer of security and prevents access to non-essential and confidential information. Many software vendors have licenses that make this possible at no cost, and this is likely to become the norm as more organizations adopt the virtual audit methodology. An organization’s risk-management software can fully document audit analysis reviews and sign-offs to mitigate fraud, ensure separation of duties and prevent access violations. Such an approach can demonstrate to external auditors that systems are in place to monitor security and manage access workflows.

Today, technology that reduces the need for on-site examinations is common, including remote teleconferencing and inventory checks. Instead of having to share physical documents in person or by courier, technology makes it possible to share files, data and documents electronically across and between organizations using shared data repositories. People involved in the process can collaborate remotely in sharing, creating and reviewing the documents.

While there are significant benefits to organizations, a virtual approach also benefits audit firms by substantially increasing efficiency, freeing up time to support more clients. Lately, there is evidence that college students with accounting degrees are less willing to go into public accounting because of working conditions, especially the hours on the road and the absence of IT-led automation that forces them to perform tedious tasks that could be done faster by software. By reducing the time auditors spend on-site and away from home as well as mitigating spikes in workloads and resulting late nights needed to complete tasks on time, audit firms can improve the ability to hire and retain staff by offering better working conditions. Organizations that require financial audits achieve similar benefits because staff time devoted to the audit is minimized. And because, in many cases, a virtual audit can enable full testing rather than sampling, it results in higher quality audits and financial statements at potentially lower costs.

The continuous audit enables audit firms to take the next step in transforming this process. Rather than doing a full audit annually, continuous auditing spreads workloads over the year to reduce as much as possible the tasks that must be performed to certify the financial statements of an organization. The underlying philosophy is similar to our approach to continuous accounting, which takes advantage of existing technology to enable the accounting staff to perform some tasks daily or weekly – rather than monthly – to avoid the stress and potential added expense of a spike in workloads during the monthly or quarterly close. Although some tasks must be done at the close of the fiscal year, ongoing random testing of an organization’s systems is more consistent with the intent of the audit process than a once-a-year approach.

that must be performed to certify the financial statements of an organization. The underlying philosophy is similar to our approach to continuous accounting, which takes advantage of existing technology to enable the accounting staff to perform some tasks daily or weekly – rather than monthly – to avoid the stress and potential added expense of a spike in workloads during the monthly or quarterly close. Although some tasks must be done at the close of the fiscal year, ongoing random testing of an organization’s systems is more consistent with the intent of the audit process than a once-a-year approach.

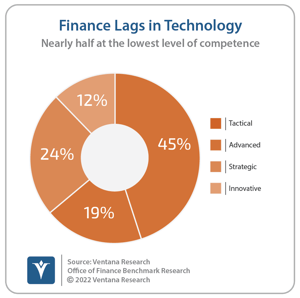

The limiting factor to the adoption of continuous audits is that, as a rule, accountants and financial executives are oblivious to technology. Our Office of Finance Benchmark Research shows that only 12% of organizations are at the highest level of technology competence, while half are at the lowest level. The continuous audit, built around a virtual audit, benefits both sides: Auditors should be geared up for it, while organizations should take steps to make this possible. Audit firms should encourage clients to make the necessary investments to support a continuous audit built around virtualizing the process because everyone involved, especially auditors, benefits.

Regards,

Robert Kugel

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).