New rules governing revenue recognition for contracts will go into effect for most companies in 2018. The Financial Accounting Standards Board (FASB), which administers Generally Accepted Accounting Principles in the U.S. (US-GAAP) has issued ASC 606, and the International Accounting Standards Board (IASB), which administers International Financial Reporting Standards (IFRS) used in most other countries, has issued IFRS 15. The two are very similar and will enforce fundamental changes in this area of accounting. The new rules will affect companies that use even moderately complex contracts in their dealings with customers. They include, for example, contracts that are structured using tiered pricing or volume discounts or ones that routinely involve modifications, such as adding or dropping users, or that allow seasonal changes to services. The changes necessitate an extensive review of an organization’s contracting and accounting policies and processes and are likely require changes to procedures and systems. Companies affected by the new rules also will need to examine their planning and budgeting processes. Those that currently use desktop spreadsheets for planning and budgeting should consider adopting dedicated planning and budgeting software in order to cope effectively with the increased complexity of planning in this new environment.

The main change in accounting for contracts stems from a new approach under which revenue (and some corresponding expense) is recognized only when customers are satisfied rather than when internally measurable events occur, such as delivery, completion of milestones or the passage of time. In some companies this will create period-to-period variability in accounting revenue and expense that will make it difficult to measure performance to plans or budgets. Thus executives will need to sort out actual-vs.-plan variances caused purely by accounting events such as a failure to receive documentation to trigger recognition, and those that reflect “real” events such as a shortfall in bookings or greater-than-anticipated labor hours.

Thus far, software vendors, consultants and accounting professionals have focused most of their attention on how the new rules will affect the accounting organization and very little on the impact they will have on the financial planning and analysis (FP&A) function. This is partly because not all companies will experience a material impact on their core accounting processes. The new rules will have little or no impact on companies whose contracts are not significant to their business operations and therefore have little or no impact on their planning and budgeting processes. Or there will be a limited impact on planning and budgeting because their contracts are relatively simple, such as the delivery of physical goods from inventory or basic annual subscriptions that do not change over their term. For them, although accounting processes will change, planning and budgeting will not. However, in some cases, planning and budgeting will become more complex because of the divergence in the timing of accounting and “real” events. FP&A organizations in these corporations need to prepare now to cope with the new environment.

The main challenge for FP&A groups in companies materially affected by the new rules is having the ability to plan corporate events (contract bookings and commission payments, for example) in parallel with accounting events, for example, forecasting when deals will close and when revenue from them will be recognized. This would be a challenge if routinely there are sufficient differences in the size and scope of contracts (which is often the case in engineering and construction, for example) or if for any other reason it isn’t possible to create an abstracted model that achieves a consistently useful, sufficiently granular approximation of the differences between “real” and accounting events. Very likely, this will be more common than many people imagine. Those who think that their planning and budgeting won’t be affected should think again.

Companies that will need to plan and budget both “real” and accounting numbers in parallel should not expect they can do it using spreadsheets. While accomplished spreadsheet jockeys may be able to create an initially serviceable model, it’s likely they and the rest of the FP&A organization will find themselves working long hours dealing with complex data imports, identifying period-to-period differences and tracking cumulative variances.

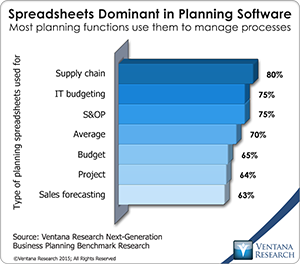

Unfortunately, odds are that many companies affected by the new accounting rules will find it very difficult to cope with planning and budgeting using spreadsheets. Our benchmark research on next-generation business planning finds that two-thirds or more companies use them to manage their budgets and other functions that can impact revenue recognition planning. Their planning models and data reside in desktop spreadsheets scattered across individual computers and file servers. In some cases, the information may also be in one or more enterprise applications. Manually pulling together these individual strands in spreadsheets on a regular basis is time-consuming and error-prone.

Financial planning and analysis groups should be  aware of their company’s exposure to ASC 606 or IFRA 15. If the new rules will have a material impact on how the company accounts for contracts, they should determine whether it will be necessary to plan and budget for “real” and accounting data in parallel. If so, and if their company currently plans and budgets using desktop spreadsheets, I strongly recommend that they look into acquiring a dedicated planning application. In addition to dealing with increased complexity, this type of software can improve the budgeting and planning processes, making them more efficient and enhancing their value as a business tool. I have noted that desktop spreadsheets are functional for individuals who create planning models and work with limited sets of data, but they are not well suited for recurring collaborative enterprise processes. Our research shows that companies that use a dedicated application more often have a process that works well or very well than those that use spreadsheets (60% vs. 47%). A dedicated application is essential to support complex planning processes. Companies need software that facilitates access to all their business units’ plans, simplifies collection of data, facilitates analysis and drilling down into detail, offers dashboards that are easy to create and modify, and supports automated and self-service reporting. This software can eliminate many barriers to effective integrated planning. We advise organizations to evaluate such products as part of a comprehensive effort to improve all facets of business planning and budgeting as well as preparing to deal with the new accounting rules.

aware of their company’s exposure to ASC 606 or IFRA 15. If the new rules will have a material impact on how the company accounts for contracts, they should determine whether it will be necessary to plan and budget for “real” and accounting data in parallel. If so, and if their company currently plans and budgets using desktop spreadsheets, I strongly recommend that they look into acquiring a dedicated planning application. In addition to dealing with increased complexity, this type of software can improve the budgeting and planning processes, making them more efficient and enhancing their value as a business tool. I have noted that desktop spreadsheets are functional for individuals who create planning models and work with limited sets of data, but they are not well suited for recurring collaborative enterprise processes. Our research shows that companies that use a dedicated application more often have a process that works well or very well than those that use spreadsheets (60% vs. 47%). A dedicated application is essential to support complex planning processes. Companies need software that facilitates access to all their business units’ plans, simplifies collection of data, facilitates analysis and drilling down into detail, offers dashboards that are easy to create and modify, and supports automated and self-service reporting. This software can eliminate many barriers to effective integrated planning. We advise organizations to evaluate such products as part of a comprehensive effort to improve all facets of business planning and budgeting as well as preparing to deal with the new accounting rules.

Regards,

Robert Kugel

Senior Vice President Research

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).