For decades I’ve heard people talk about cutting audit costs to reduce administrative overhead but based on my observations, I was skeptical — mostly because, until recently, the documented success stories haven’t been about going from good to great so much as going from awful to average. That’s changing. I recently wrote about a company that had set out to cut its external auditor’s fees. The benefits it had accrued are significant, including a reduction in staff time devoted to the audit. I also explained why cutting audit fees wouldn’t be easily duplicated in every company.

In the months since, I’ve come to believe that reducing audit costs ought to be a priority for the CFO and an important ongoing performance metric for most finance and accounting organizations. While cutting audit fees can be problematic, almost all companies can realize a significant reduction in staff time devoted to the audit and its related expenses. Because of its impact on the organization, improving the efficiency of the external audit should be top-of-mind for the CFO and controller. Moreover, performance in these roles should be measured in terms of hours spent by staff as well as direct expenses related to the audit. It’s not just the audit process that would benefit. Actions that improve audit execution will simultaneously improve the overall performance of the department. The people, process, data and software issues that burden audit compliance workloads hamper all aspects of the department’s performance.

As with almost all such undertakings, sustainably reducing staff time and related costs related to the audit requires a change-management initiative.

Reducing the internal costs of audit compliance isn’t easy. If it were, organizations would have done so a long time ago. As with almost all such undertakings, sustainably reducing staff time and related costs related to the audit requires a change-management initiative. This effort involves people and process changes as well as attention to IT systems and data management. It’s highly unlikely that an organization can achieve meaningful audit cost transformation in a single 90-day sprint. It’s more likely to be an ongoing multi-year evolution. The transformation must be deliberate, managed as a set of quantifiable final objectives and measurable interim goals.

The key to cutting audit costs is adopting what I call an “open-book” approach that gives external auditors full, read-only access to the IT systems relevant to the audit — of course within reasonable limits. Here’s a quick summary of what an open book approach looks like:

- First, the company provides the auditor full access to the company’s general ledger systems with just a few exceptions related to matters of confidentiality, such as the payroll detail. Enabling the external auditor to access the system off-site (an attractive option) is easier to do with a cloud-based ERP application.

- Second, the company offers the auditor full access to the close management system, making it possible to confirm that cash ties, for example, and to view the system logs to check for anomalies. This also means the company needs to have a close management system deployed, not just a spreadsheet checklist and email communications.

- Third, the company gives the auditor access to any other relevant software system of record that adds efficiency and transparency to the process and that doesn’t pose confidentiality issues. This can include risk management software. Such software can pinpoint fraud, separation of duties and access violations. And it can include systems that monitor security and manage access workflows.

- And fourth, the company makes a document sharing system available for remote viewing of non-confidential documents the auditor needs. The accounting staff likely will know what needs to be available, including certifications, working papers and status reports related to issues raised in the previous audit.

Here’s where the savings come in. The open-book approach that technology makes possible cuts everyone’s workload. For instance, there’s no lengthy “provided by client” (PBC) request for data and documents that the accounting staff must curate and collate. Seemingly endless interruptions by the auditors to handle information requests are a thing of the past. The data is in digital format already, which simplifies the external auditor’s job — no more rekeying or poring over paper documents, which takes time and costs money. Instead, the auditor saves time by sampling directly from the general ledger and other electronic systems. And because the auditor can access systems and documents remotely, an organization can cut on-site time and related costs — maybe significantly.

Of course, this is the ultimate objective. Getting there may involve, for example, acquiring new software, such as a close or risk management system, simplifying the structure of financial management systems or implementing end-to-end process and data management. The end-to-end initiative is a core component of continuous accounting that ensures data quality.

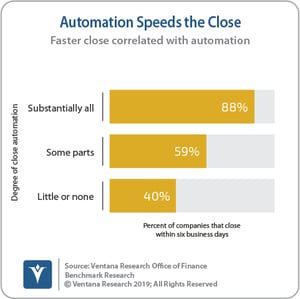

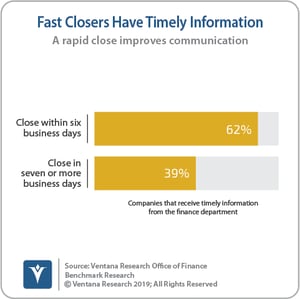

Each of these initiatives pays dividends beyond cutting audit costs. For example, our recent benchmark research on the Office of Finance confirms the value of using a close management system: 88% of organizations that automate substantially all of their close processes can complete that process within six business days compared to 59% that have automated some parts and just 40% that apply little or no automation. Beyond efficiency benefits, closing sooner enables the department to provide financial and management data to the rest of their organization sooner. The research finds that a solid majority (62%) of those companies that close within six business days provide timely information compared to only 39% of those that take longer.

recent benchmark research on the Office of Finance confirms the value of using a close management system: 88% of organizations that automate substantially all of their close processes can complete that process within six business days compared to 59% that have automated some parts and just 40% that apply little or no automation. Beyond efficiency benefits, closing sooner enables the department to provide financial and management data to the rest of their organization sooner. The research finds that a solid majority (62%) of those companies that close within six business days provide timely information compared to only 39% of those that take longer.

It’s not straightforward for organizations to address the people issues that organizations must overcome to streamline audit compliance. Orchestrating change is rarely easy for executives and managers. This is particularly true for accounting organizations because those attracted to the profession usually like sticking to routines. On the other hand, the new generation of accountants joining the workforce are likely to welcome an approach that minimizes tedious repetitive tasks and enables them to do work that requires their training and intellect. Being able to attract and retain top talent provides lasting benefits. Moreover, having a cooperative relationship with the auditor will be necessary to achieve meaningful internal savings. In theory this is always possible but history and organizational culture may make it difficult.

be necessary to achieve meaningful internal savings. In theory this is always possible but history and organizational culture may make it difficult.

As a pragmatist, I understand that some executives may be reluctant to jump into a full open-book approach. But it doesn’t have to be all or nothing. Many companies will find that methodically eliminating roadblocks to an open-book audit will make the department more efficient, improve the quality of its financial reporting and reduce compliance and reporting risks.

CFOs and controllers must make cutting audit costs a priority. They should take a leadership role in transitioning the department to a new external audit approach and a focus on continuously improving the efficiency of the process. They must also be prepared to invest in systems that lead to these efficiencies. In my opinion, an open-book approach to the external audit is not simply “nice to have.” Significantly reducing the internal costs and audit fees devoted to compliance frees up time and money that can make your organization more competitive and sustainable.

Regards,

Robert Kugel

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).