For years I’ve viewed with skepticism the claim that one technology or another will reduce audit costs. For one, there’s rarely a silver bullet. An array of moving parts drive audit fees. For example, the complexity of the corporation, accounting data management and the audit staff’s familiarity with the industry and the company all affect the time auditors must spend. Also, most of the time I’ve found that achieving significant savings was not the result of going from good to great, but from fixing deep-seated issues. If a company’s books and accounting practices are a mess, it can achieve considerable savings simply by cleaning up its act. In this circumstance, technology can play a part of a broader initiative that addresses the people, process and data management elements that are behind the mess.

However, I recently attended a session at a user group meeting where a company described how it was able to cut its audit costs — significantly. After listening and considering what was presented, I’ve concluded that drastic improvement is possible, even if you already have a tight accounting organization. And technology plays a key role.

In this case, the company was able to cut its direct audit costs to about half of what it had been. It also was able to free up a substantial amount of staff time that had been devoted to the audit. The key elements of its savings were limiting the “provided by client” (PBC) request to less than a page and reducing the outside auditor’s onsite time by about half. The auditor was able to perform the audit in far less time than it had in the past.

A prerequisite to achieving this degree of savings is having a cooperative rather than confrontational relationship with the auditor. This is always theoretically possible but history and organizational culture may make it difficult to take this route. There also may be some hesitancy on the auditor side, particularly work done for U.S. public companies. The Public Company Accounting Oversight Board (PCAOB), established by the Sarbanes-Oxley act, oversees audits and auditors. A cooperative relationship between a company and its auditor may be viewed as “cozy” and therefore suspect. If the company-auditor relationship is built on transparency, though, an organization should find it easy to justify a cooperative relationship.

At the user group meeting, the company laid out how technology enabled it to cut the auditor’s onsite time and substantially shorten the PBC list. It did so by:

- Providing to the auditor a license enabling full access to the company’s general ledger with a few exceptions related to confidentiality maters (such as the payroll detail).

- Granting view access to the expense management system.

- Giving the auditor access to view the close management system, enabling him or her, for example, to confirm that cash ties and to view the system logs to check for anomalies.

- Providing a document storage system for remote viewing of non-confidential documents that are likely to be of interest to the auditor.

Technology and an open-book relationship mean that the auditor does less work than typically is the case with a confrontational approach. The latter frequently results in a long request for data and documents. Often organizations provide data in PDF files that are not machine readable so they must be rekeyed by the auditor for analysis. Other information is in paper documents that must be copied and scanned. Usually, the document request is incomplete and initially may not be completely fulfilled by the company, leading to additional back-and-forth that consumes the time of both the auditor and the accounting staff.

By contrast, the company presenting its case noted that because the auditor can access data and documents directly, he or she spends far less time cataloging requirements. Both parties spend less time providing and consuming documents. There is no data dump into documents that cannot be consumed electronically. The auditor samples directly from the general ledger system, saving time. Because the auditor can access systems and documents remotely, there’s no need to come on-site until the final stages of the audit. In this specific  case, instead of 10 business days on site, the company’s auditor now spends four days, with a commensurate reduction in travel expenses. Moreover, the auditor does incremental audits over the fiscal year, so issues are resolved sooner and don’t pile up until the final audit.

case, instead of 10 business days on site, the company’s auditor now spends four days, with a commensurate reduction in travel expenses. Moreover, the auditor does incremental audits over the fiscal year, so issues are resolved sooner and don’t pile up until the final audit.

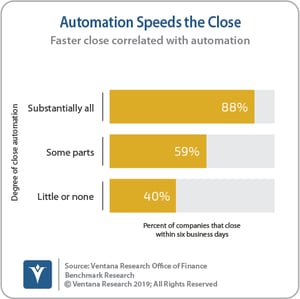

The sort of systems and processes that can reduce audit fees also can provide other business benefits. For example, our Office of Finance benchmark research demonstrates that companies that automate their close process are able to close sooner. Almost all companies (88%) that have automated substantially all of their close process can close within six business days, compared to 59 percent that automate some parts and just 40 percent that automate little of none. Closing sooner means that financial and managerial analysis and reporting is completed sooner, enabling executives and managers to seize opportunities and address issues sooner. For their part, auditors are able to use the logs of these systems to confirm that work was performed and that any issues were resolved and attested.

I’m certain that an open-book, cooperative approach to auditing that utilizes technology to significantly reduce workloads can cut audit costs. However, I’m not sure how reproduceable this example is today. Not every company will feel comfortable providing unrestricted access to its records. This example is a midsize company with relatively straightforward systems and business processes. Some businesses are complex and inherently messier, so it’s possible that rather than saving time, auditors would spend the same amount of time looking into more data and resolving more questions. The company in question uses a single cloud ERP system, which simplifies access. The company uses electronic systems almost universally throughout the business so almost all needed data is accessible by the auditor in digital formats. Complications can arise when work is done in a vast array of desktop spreadsheets that may not be fully accessible. And an auditor may be loath to accept any arrangement that materially lowers its fees since jobs and livelihoods are at stake.

All the above considerations aside, I believe that the company I saw is an example of the future direction of the audit process. Technology can play a key role in reducing audit fees and the time spent by the accounting staff on the audit by making their accounting more transparent and therefore easier to work with. Computing systems increasingly provide transparency that has greater business value than the supposed security of opaque systems and processes. Opaque systems rely on the old auditing adage: “The threshold of materiality rises exponentially as deadlines loom.” In other words, making the audit process a paper chase is worthwhile if a company is uncertain of the quality of its accounting or has something to hide.

Digital technologies can improve the quality of a company’s books and lessen anxiety around having an open-book relationship with the auditor. For example, Ventana Research advocates using an approach we call “continuous accounting” that builds quality into accounting processes. In coming years artificial intelligence (AI) will play an increasing role in ensuring accounting data quality. Although it may sound futuristic and whiz-bang, AI is already being brought to bear, for example, on the mundane task of ensuring that accounting entries are accurate and complete at the time of the entry without resorting to tedious programming or enduring an overload of false positives that slow processes down.

The use of technology to reduce audit costs is part of our research agenda and we will be following its evolution over the coming years. I recommend that all CFOs and controllers consider how their company can reduce its audit costs, both the direct fees and the indirect cost of unproductive staff time.

Regards

Robert Kugel

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).