In preparing this research note I took the precaution of searching “value-based planning” to see what came up. Over the years, the term has been used in several contexts each with different shadings. By my definition it’s an approach to planning and budgeting that maximizes the long-term value of an organization by considering all its objectives – not just the financial targets. Value-based planning is a more effective management tool for executives because it defines objectives in terms of resources used and outcomes achieved, not just the financial outcome. Value-based planning is only possible when it is fully supported by the senior leadership team and only feasible using software that can integrate operational planning and financial budgeting.

In one of its earliest forms, value-based planning was associated with the concept that managements must focus on creating shareholder value. This idea acknowledged the schism that can exist between the short-term motivations of a self-interested executive management team and the interests of the investors in that corporation. To create value for shareholders, executives are obliged to establish objectives in terms of their financial impact measured by using a discounted cash flow method. By applying this discipline, overpaying for some acquisition or embarking on some vanity project with limited economic potential would be discouraged because these investments couldn’t be justified by an objective financial measure of value. And, since share prices are considered to be the result of the equity market discounting the value of all future cash flows, for publicly traded companies, measurement of shareholder value has most often been equated with its share price behavior.

By the 1980s, management theorists in the English-speaking world recognized that objectives based solely on financial parameters were inadequate and often proved counterproductive. Too often they encouraged a short-term mindset in corporate executives. Moreover, a financials-only approach runs counter to a basic organizational principle that goal-setting based on a single metric is almost guaranteed to produce suboptimal results. Successfully managing a business is a matter of correctly evaluating trade-offs because resources are always limited. Neglecting product quality, brand equity or safety might save money in the short run but almost always diminishes the long-term value of an enterprise.

The balanced scorecard, first used by an electronics manufacturer in the 1980s and later espoused by business school professors, was an expression of that principle. It recognizes that in setting objectives and rewarding performance corporations must balance multiple objectives including customer satisfaction, market leadership, corporate reputation, and employee satisfaction, to name a few. Rather than focusing solely on short-term financial gain, balancing these multiple objectives almost always results in maximizing the long-term value of a corporation. At the same time, history has repeatedly shown that ignoring or minimizing the importance of achieving a necessary return on invested capital ultimately causes companies to lose competitiveness and even fail.

Value-based planning, in my context, is an approach to corporate planning and budgeting that integrates operational planning and financial budgeting; a forward-looking exercise that incorporates “things” not just money. Things like headcount, kilowatt hours used, less-than-truckload shipments, invoices processed and so on. This is more effective because, for one, those responsible for a business unit think about their requirements and objectives mainly in terms of things they need to achieve and the things they use to achieve those objectives. Money is an abstraction of those things.

Value-based planning utilizes models that enable budget owners to plan in terms of those things and then have the model automatically generate a financial budget from those units based on assumed prices. This approach is better aligned to how business owners think and therefore planning and budgeting is faster and easier for them. Ventana Research asserts that by 2025, fewer than one-third of organizations will have adopted value-based planning, but those that do will outperform their peers in achieving their objectives and long-term strategy. Moreover, while quantifying financial performance is essential to the success of an organization, it’s equally important to plan and measure operating performance. And, reflecting the concept  of the balanced scorecard, measuring operating performance not just in terms of the efficient use of inputs and outputs but also the effectiveness with which the business unit operates – effectiveness measured in terms of customer satisfaction, employee safety and measures of sustainability, to name a few.

of the balanced scorecard, measuring operating performance not just in terms of the efficient use of inputs and outputs but also the effectiveness with which the business unit operates – effectiveness measured in terms of customer satisfaction, employee safety and measures of sustainability, to name a few.

Using value-based planning, budget discussions can focus on the key quantifiable resources such as headcount and production capacity, not just abstract accounting percentage changes in budget allocations. Financial objectives are the key consideration in creating plans and budgets. Financial control and financial returns are essential to long-term success, but they shouldn’t be the sole measure by which to judge an operating plan.

I’ve written before about making budgeting easier for the budget owner, an objective that is consistent with value-based planning. Typically, preparing a financial budget is time-consuming and anxiety-ridden for managers. They must determine the resources required to meet their business objectives (which usually begin as a top-down directive) and then translate those resources into monetary terms, often in a non-intuitive structure aligned with the company’s general ledger. This process is designed around the needs of the finance organization and not for line-of-business managers and executives. Even today, this method of budgeting is the result of the time and resource constraints of an earlier age when the available technology – notably paper ledgers and adding machines – limited corporate planning to setting an annual budget. Today, dedicated planning applications support a modeling approach that, using established techniques, can immediately translate things into monetary terms and allocated to general ledger accounts. This serves the needs of executives and managers as well as the finance organization and can take less time and effort compared to desktop spreadsheets.

Driver-based modeling is an essential element of a process that supports value-based planning. Driver-based modeling pinpoints the most important factors that determine an organization’s ability to achieve its strategy and objectives, either an entire company or a business unit. For example, the ability of a product company to execute a low-cost strategy depends on minimizing the cost of manufacturing a product. In this example, cost is mainly a function of material costs, labor cost and labor efficiency, machine efficiency and uptime, and scrap rates. Planners use these drivers to construct operating and financial plans for business units. Driver-based modeling simplifies the planning process by isolating the 20% of factors that drive 80% of the results. This type of modeling is a better representation of how an organization functions compared to a purely financial plan and it simplifies the job of creating an integrated operating and financial plan for the business owner because the model incorporates the financial implications of the key drivers, such as labor and material costs.

Value-based planning also makes the periodic performance review process more of a management tool because it considers both operational and financial results rather than emphasizing the latter. Because things and money are planned and tracked in parallel, the root cause of divergences from plan are clearer than when reviews are primarily about financial variances. Driver-based modeling helps in this regard because defining the key drivers isolates the factors that a manager can control, such as labor efficiency, scrap rates and machine uptime, from those that he or she cannot, such as material prices and – to a large extent – labor costs.

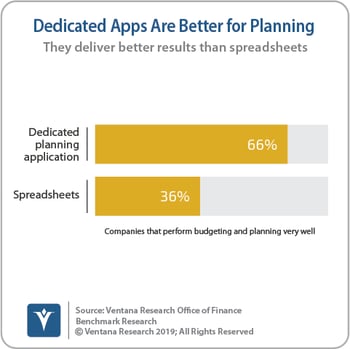

Value-based planning isn’t feasible for a midsize or larger organization that uses desktop spreadsheets to support its forecasting, planning, budgeting, analysis and review cycles. Unfortunately, our  Office of Finance benchmark research found that 58% of companies use spreadsheets to support their planning and budgeting. Spreadsheets are two-dimensional grids and therefore cannot easily incorporate modeling things and their financial impact in parallel. Being two-dimensional, it is extremely cumbersome to consolidate a set of business unit plans, each with their multiple dimensions (such as labor and commodity costs, product hierarchies, exchange rates and organizational structures) into a coherent whole. Partly for this reason, our research found that 66% of companies that use a dedicated planning application have a process that works well compared to 36% that rely on spreadsheets. In theory, you can do anything in a spreadsheet if you have enough time, but time is the key constraint that makes value-based planning infeasible for spreadsheets.

Office of Finance benchmark research found that 58% of companies use spreadsheets to support their planning and budgeting. Spreadsheets are two-dimensional grids and therefore cannot easily incorporate modeling things and their financial impact in parallel. Being two-dimensional, it is extremely cumbersome to consolidate a set of business unit plans, each with their multiple dimensions (such as labor and commodity costs, product hierarchies, exchange rates and organizational structures) into a coherent whole. Partly for this reason, our research found that 66% of companies that use a dedicated planning application have a process that works well compared to 36% that rely on spreadsheets. In theory, you can do anything in a spreadsheet if you have enough time, but time is the key constraint that makes value-based planning infeasible for spreadsheets.

Value-based planning also requires a change in mindset at the senior management level because it entails a major departure in planning, budgeting and measuring performance. This type of change must begin with a clear direction from senior management. Value-based planning also should be part of a redefinition of the mission of the financial planning and analysis group, which I outlined recently in a short video.

From CEOs on down the line, people have been complaining for decades about having to prepare the annual budget. Largely this is because the process is time-consuming and burdensome without delivering much value to heads of business units or senior executives. A value-based planning approach addresses these complaints by using technology to streamline the process and shifting the focus from a purely financial orientation to one that also incorporates measures of operational efficiency and effectiveness. FP&A organizations that want to increase their strategic value to the finance department and the entire organization should develop a program and business case for adopting value-based planning.

Regards,

Rob Kugel

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).