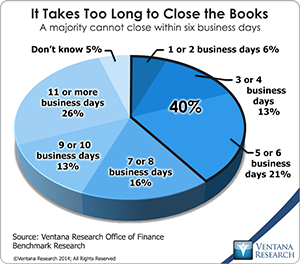

In our Office of Finance benchmark research 60 percent of participants said it takes their companies six or more business days to complete their quarterly close; that exceeds the best practice benchmark of five days. Consultants, academics and vendors have stressed the importance of shortening the close for almost a quarter of a century. The main reason for doing so is to provide executives and managers with timely information about the company’s performance. Yet our research shows that it’s taking longer for companies to complete their close than it did a decade ago: On average they now finish the monthly process in 6.8 days, compared to 6.5 days, and complete the quarterly close in 8.0 days vs. 7.5 days. The research suggests that the main reason for this increase is that companies use outdated manual close processes, which often are poorly executed and rely heavily on spreadsheets.

For companies that take more than a week to close their books, shortening the close represents an opportunity to improve how well they handle all finance and accounting processes. That’s because the close is a useful benchmark of the overall effectiveness of a finance organization. Here’s why: Imagine two companies that on paper are nearly identical – they are about the same size, compete in the same industry, operate in the same geographies, and have the same ownership structure, the same number of ERP systems and the same degree of centralization of the accounting function. One closes in three business days; the other in eight. In theory, having nearly identical requirements, resources and constraints, the two should close within about the same interval. In the one that takes longer, however, there is likely some combination of overly manual processes that are poorly executed, inadequate financial management systems and heavy use of desktop spreadsheets to compensate for these inadequacies. It also may be a measure of executive complacency or an unwillingness to tackle the issues. Addressing the root causes of any of them will not only help accelerate the close but also, because the root causes likely have a negative impact on other departmental processes, probably will improve overall departmental performance.

to close their books, shortening the close represents an opportunity to improve how well they handle all finance and accounting processes. That’s because the close is a useful benchmark of the overall effectiveness of a finance organization. Here’s why: Imagine two companies that on paper are nearly identical – they are about the same size, compete in the same industry, operate in the same geographies, and have the same ownership structure, the same number of ERP systems and the same degree of centralization of the accounting function. One closes in three business days; the other in eight. In theory, having nearly identical requirements, resources and constraints, the two should close within about the same interval. In the one that takes longer, however, there is likely some combination of overly manual processes that are poorly executed, inadequate financial management systems and heavy use of desktop spreadsheets to compensate for these inadequacies. It also may be a measure of executive complacency or an unwillingness to tackle the issues. Addressing the root causes of any of them will not only help accelerate the close but also, because the root causes likely have a negative impact on other departmental processes, probably will improve overall departmental performance.

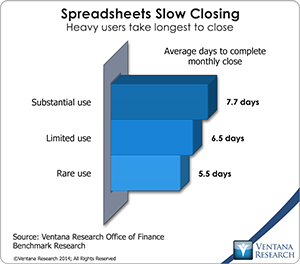

For example, consider the ill-advised use of desktop spreadsheets in departmental processes, which is a common cause of poor performance of the close. Our research correlates the degree to which companies use spreadsheets in the close with how long it takes a company to complete the process. Those that are substantial users on average take 7.7 days, more than one day longer than those that limit their use (6.5 days) and more than two days longer than those that rarely use them (5.5 days). One reason for this disparity is that spreadsheets are inherently error-prone, and thus the work product from spreadsheets must be checked and validated, which is a time-consuming process.

For example, consider the ill-advised use of desktop spreadsheets in departmental processes, which is a common cause of poor performance of the close. Our research correlates the degree to which companies use spreadsheets in the close with how long it takes a company to complete the process. Those that are substantial users on average take 7.7 days, more than one day longer than those that limit their use (6.5 days) and more than two days longer than those that rarely use them (5.5 days). One reason for this disparity is that spreadsheets are inherently error-prone, and thus the work product from spreadsheets must be checked and validated, which is a time-consuming process.

The use of spreadsheets in recurring corporate processes may be the immediate cause of a slower than necessary close, but their use often is the result of bigger issues that should be addressed. For example, heavy use of spreadsheets may stem from poorly structured IT systems. There might be duplicate data sources that must be reconciled or calculations, which could be done automatically in a more capable system but instead are performed in spreadsheets and therefore must be constantly checked for errors. Similarly spreadsheets may be used to collect and derive numbers from multiple systems instead of automating the integration of data as it is passed between systems; this also consumes the time of skilled professionals needlessly. Identifying and addressing this root cause of a tardy close will improve the execution of most finance and accounting department processes. Maintaining data integrity by automating calculations within all financial systems and automating all links between them can improve the quality of any financial and management analysis, reporting, forecasting and planning.

Fixing IT system problems might also inspire broader attempts to improve finance department performance, including those that are the result of a complacent, “we’ve always done it this way” approach. Even something as basic as failing to rethink the process can lengthen the close. It’s not “cheating” to close subledgers before the end of the period, provided it’s done consistently and doesn’t inherently result in a misstatement. Balancing workloads during an accounting period is good management. Setting higher thresholds for reconciliations can save a substantial amount of time without adversely affecting the quality of a company’s financial statements. A relentless drive to shorten the close also requires executives to rethink and question a lot of “givens” that routinely degrade their performance. “Relentless” means that it becomes a high priority that challenges a sense that “we’re too busy to improve efficiency.”

Our research on speeding the close finds that the most effective strategy for shortening the process is to control the process consistently. A large majority (71%) of companies said that doing this enabled them to shorten their close; this is by far the most frequently cited source of improvement. Continuous process improvement is an approach long used in manufacturing to improve the quality of output and, by eliminating the need for scrap and rework, enhancing process efficiency. The same applies in finance departments. Continuous process improvement requires frequent reviews of performance and immediately addressing issues that arise from these reviews. The frequency of these reviews is important: In our research two-thirds (67%) of companies that review their close process monthly said they were able to achieve their goal of shortening their close, compared to half of those that did it quarterly and one-fourth (26%) of those that do not do such reviews.

I propose that every company that takes more than a business week to complete its monthly or quarterly close should set a goal of reducing the time by at least two days over the next three years. If it now takes 11 or more days, the goal should be four fewer days. Making this effort is worthwhile for three reasons. Shortening the close enables a company to provide vital financial and managerial information sooner, and it increases efficiency. Moreover – and possibly of even more value – the process of identifying the issues and bottlenecks that prevent a faster close is also likely to point to other issues involving people, process, information and technology that hamper the finance organization. Fixing the close process issue can be an excellent diagnostic tool for assessing anything else that might be ailing Finance.

Regards,

Robert D. Kugel CFA

Senior Vice President, Research

Follow Me on Twitter @rdkugelVR and

Connect with me on LinkedIn. www.linkedin.com/in/robertkugel

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).