Price and revenue optimization (PRO) software uses analytics to help companies maximize profitability for any targeted level of revenues. PRO utilizes data about buyer behavior to gauge individual customers’ price sensitivity and predict how they will react to prices. It enables users to charge buyers who appear to be less sensitive more than those who appear more price-sensitive. PRO is a significant departure from inward-focused, single-factor pricing strategies such as cost-plus pricing or, in the case of financial services, risk-based pricing (using a borrower’s credit score, for example). Instead it offers a multifaceted customer-centric analytic approach to pricing built on analysis of large sets of data.

credit score, for example). Instead it offers a multifaceted customer-centric analytic approach to pricing built on analysis of large sets of data.

Price and revenue optimization is a natural fit for the application of big data analytics. Our benchmark research on challenges in big data shows that three-fourths of companies are addressing more than 10 gigabytes of data per day and 10 percent are deal daily with a terabyte or more. Financial services companies in particular can benefit from big data analytics because their core products are essentially numbers. For them, analytics involves sifting through large data sets to collect characteristics of consumer behavior that will enable them to identify customer segments and quantify their price sensitivity. These complex calculations require software designed for the purpose. Big data analytics software can help users manage more granularly the process of defining offers to customers (and the levels of discretion they allow to account managers and sales people to set prices) as well as the terms and conditions of the transaction. Upon identifying characteristics that influence buyers’ price sensitivity companies then combine the most relevant factors to present a price that will enable them to optimize revenue and profits from those customers.

Nomis Solutions provides PRO software and services to financial services companies, including banks, automobile credit providers and credit card processors. In past years at its annual user conference, the company has focused on the science and technology behind its product, as I’ve noted. Those sessions were useful in providing attendees with a deeper understanding of “the why behind the what” of the applications’ capabilities.

Taking a somewhat different approach this year’s conference focused on the challenges that the financial services industry will need to address over the next several years and how information technology generally – and price and revenue optimization software specifically – can help these institutions address them. Presenters at the Nomis Forum covered three main issues facing financial services businesses:

- Increasing velocity and volatility of interest rates

- Disruptive sources of competition in financial services

- Expanded regulation of financial services businesses.

Those charged with setting prices in financial institutions have been operating in a relatively benign environment for the past few years. Interest rates in many of the developed world economies have remained relatively steady and low in inflation-adjusted terms by historical standards; this simplifies the pricing of loans and credit. The recent environment of low interest rates and low volatility has muted the need for the capabilities found in PRO software, although financial services companies that have deployed PRO have improved their results measurably. However, it’s likely that the interest rate environment will transition to a more dynamic phase within a few years. Technology can enable financial institutions to operate more effectively in that kind of interest rate environment, helping financial services companies be more effective when interest rates begin to rise and fluctuate. It can do so by enabling them to automate analytics and reporting as well as facilitating management of the related data. This makes it easier for a financial institution to adapt fast to a challenging atmosphere and set prices in a way that best matches its strategic objectives (such as to be a market share leader in specific product categories or to maximize returns on risk-weighted assets). Using price and revenue optimization rather than simplistic risk-based pricing can provide a competitive advantage in achieving higher returns on assets and lower costs of capital.

However, such technology may present challenges to established financial services organizations. As it has been in many industries, it is becoming a disruptive force, especially as innovators use the Internet and evolving computing devices to change the competitive landscape. The financial services business is feeling the impact of new approaches to traditional methods. Deposit banks, mortgage companies and other lenders as well as major credit card companies all face challenges from entrepreneurs seeking to supplant established business systems. There are new formulations of finance in areas such as peer-to-peer lending (for example, Lending Club), purely online banking establishments, mobile payments systems (such as Apple Pay) and crypto currencies (Bitcoin). To date these new formulations haven’t achieved significant penetration, but when technology-driven market disrupters arrive, Andy Grove’s cautionary advice – “Only the paranoid survive.” – is worth heeding. The upstarts have attracted substantial amounts of investment capital, giving them parity with established players in terms of a low cost of capital and the ability to keep trying.

In assessing the challenge from disruptive innovators, Nomis founder Robert Phillips insisted that financial services incumbents are not defenseless. They are able to match innovators in matters of convenience and (to some degree) cost, two areas where companies such as Amazon, Netflix and online travel booking services were able to use these aspects to quickly displace well-established companies. Existing financial institutions have been adopting technology by developing it internally or by acquiring technology-enabled disruptors. For example, in the United States the camera-equipped smartphone took advantage of the 2003 law that eliminated the requirement that physical checks must be returned to their makers to enable people to “deposit” checks into their account without having to go to a bank or an ATM. Traditional financial services companies have heavy compliance costs and considerable overhead that give upstarts and advantage, but they also have some advantages of scale.

Philips cited two major areas of competitive differentiation. One favoring new entrants and the established organizations. Incumbents are most vulnerable to disruption because typically they are slower in reacting to customers and ponderous in managing processes. Retail and small business banking is a consumer market, and today consumers in developed countries increasingly want transactions to be fast and hassle-free. On the other hand, incumbents have a wealth of information about their about customers, their assets and their past behavior that they can use to optimize pricing in every aspect of their business as well as to improve their customers’ experiences. Using software to manage rates charged or offered is a way to quickly provide quotes to prospective borrowers and depositors while providing effective controls on how front-line representatives set rates. Upstarts that have less of this information available will have to rely more on risk-based pricing.

Increased regulation since the 2008 financial crisis is another major challenge for financial institutions in the developed world. Its purpose has not just as an attempt to prevent future debacles but, particularly in the United States, to promote fairness. For cultural reasons, demanding different prices from some customers or raising prices during periods of peak demand is a sensitive topic in many developed economies. Tightly regulated financial services companies are more vulnerable to charges that some protected groups are hurt in the price-setting process and therefore subject to fines and demands for restitution. One advantage that companies using PRO software have in defending against charges of unfairness is that it makes the price-setting process transparent and based on objective measures related to their willingness to pay.

Price and revenue optimization is a strategic business technique that has conclusively demonstrated its value in travel and leisure, retail and industrial businesses. It is steadily gaining traction in financial services. Yet from discussions with existing users I find that it is rarely easy to implement from a management and process standpoint. One important reason is that the results of the analysis of customer behavior often defies common sense. The use of big data analytics to assess and quantify the drivers of customer decision-making enables a company to apply a more nuanced view of the often complex factors that influence customer decisions. From this analysis it can segment its prospects more accurately than by using simplistic assumptions (that is, what “everybody knows” to be true). For example, it may not be necessary to offer loyal customers the lowest price. Other inducements may be more important to them and may even be costless to the financial institution or seller – for example, maintaining an ongoing relationship or not having to spend time shopping around. Indeed, one advantage of PRO is that it’s often counter-intuitive and therefore offers strategies unavailable to less well informed competitors. PRO also is an operating methodology so it’s not easy to implement the management and process changes necessary to utilize the technique, especially in larger organizations. Nonetheless, companies that recognize its advantages and put it into practice can obtain a competitive advantage over competitors that aren’t able to overcome institutional inertia.

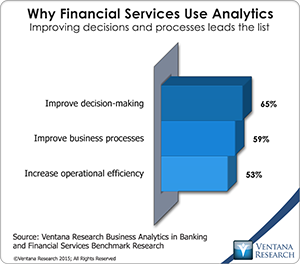

I recommend that companies, especially those in the financial services industry, explore the benefits of using price and revenue optimization tools. It is worth remembering that technology has long been a driver of innovation and change in financial services. Our research on the use of analytics in banking and financial services shows that financial services companies are looking for analytics that will improve their decision-making and business processes as well as enhance their operational efficiency. They want analytics to enhance their competitiveness and provide a strategic advantage. PRO is a technology-driven technique that can underlie a more intelligent and strategic approach to pricing.

services industry, explore the benefits of using price and revenue optimization tools. It is worth remembering that technology has long been a driver of innovation and change in financial services. Our research on the use of analytics in banking and financial services shows that financial services companies are looking for analytics that will improve their decision-making and business processes as well as enhance their operational efficiency. They want analytics to enhance their competitiveness and provide a strategic advantage. PRO is a technology-driven technique that can underlie a more intelligent and strategic approach to pricing.

Regards,

Robert Kugel – SVP Research

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).