Because my research practice is centered on important business issues where technology is a key part of a solution, my written perspectives tend to focus on technology. However, it’s almost never the case that a company can just implement some application and fully resolve a business issue. Some progress may be achieved by using more effective tools, but in most cases results will fall short of what’s possible unless people, process and information issues are addressed as well. This is especially true for the accounting close.

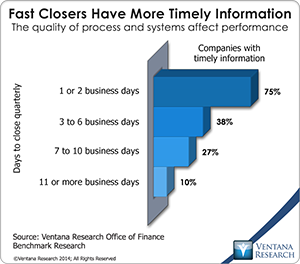

It is generally agreed that companies should close their books  within one business week. On important reason to do that is that prompt closing enables them to make essential performance metrics available sooner to executives and managers. Our benchmark research on the Office of Finance confirms this correlation. Three-fourths (76%) of companies that close their books in one or two business days said they have timely information available to run the company, compared to just 10 percent of those that take more than two business weeks to complete the process. The timeliness of performance-related information is an important factor in how nimbly a company is able to respond to challenges or opportunities. However, despite nearly universal agreement that it’s important or very important to accelerate their company’s close (for 83% of companies in our research on developing a fast close), we also found that companies on average are taking a day longer to close their quarterly books than they did a decade ago. Using ineffective technology certainly plays a role, as I’ve discussed, but a poorly executed process is just as important a barrier to closing quickly.

within one business week. On important reason to do that is that prompt closing enables them to make essential performance metrics available sooner to executives and managers. Our benchmark research on the Office of Finance confirms this correlation. Three-fourths (76%) of companies that close their books in one or two business days said they have timely information available to run the company, compared to just 10 percent of those that take more than two business weeks to complete the process. The timeliness of performance-related information is an important factor in how nimbly a company is able to respond to challenges or opportunities. However, despite nearly universal agreement that it’s important or very important to accelerate their company’s close (for 83% of companies in our research on developing a fast close), we also found that companies on average are taking a day longer to close their quarterly books than they did a decade ago. Using ineffective technology certainly plays a role, as I’ve discussed, but a poorly executed process is just as important a barrier to closing quickly.

Closing the books is a highly definable, repetitive procedure, similar in that way to a manufacturing process. In both cases, attention must be paid to the design of the process. It must be examined step by step to determine, for example, whether there unnecessary or redundant steps and they are in the most efficient sequence. The execution of the process must be evaluated to confirm that handoffs between individuals are always crisp and that exceptions are handled quickly. As in manufacturing, it’s important to take a total quality management approach – one in which design of the process and related methods eliminates as many sources of defects as possible. In the case of the close, the process should be supported by systems designed to prevent errors from occurring. Building quality into the process minimizes the need to spend time discovering the source of a mistake and then fixing it. On average research participants estimated that they could save one to two days in closing if all errors were eliminated.

The financial close is a complex process so it’s not easy to spot the sources of bottlenecks and root causes of defects without analyzing it in detail. Most people involved can describe their process at a high level, but those taking more than a business week to complete the close need to compile a complete definition of their process. This is more difficult than it might seem. Collectively, the accounting organization performs hundreds of steps (larger or more complex companies may have to do thousands) as well as hundreds of exception routines. Finance executives and accountants in these organizations usually don’t realize how many steps and processes there are. They often are surprised by the number of spreadsheets that they use in the process. Software that can compile a full list of steps, their precedents, exceptions and handling and the applications or spreadsheets used for that step can help automate the process, and our research shows that automation saves time. While defining all the steps is a painstaking process, it’s necessary to achieve even bigger time savings.

A carefully detailed examination of close processes may find that changing the sequence of close-related tasks is another way to accelerate the completion of the process. For example, rather than performing an entire month’s work after the end of the period, it may be possible to reduce the crush of work by spreading it out over the month into a weekly or biweekly task. Another approach many companies use is closing subledgers before the end of the period. If there is no material change in the amounts between that point and the end of the period (applied consistently) it will not distort the company’s financial results. Even if starting these tasks earlier has no impact on the total hours of work that must be performed, the object of closing sooner is to get important information to the rest of the organization as soon as possible.

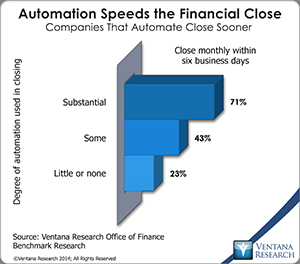

Still, technology has an important role in making process improvement feasible. A CFO and controller may be reluctant to embark on a major overhaul of their close because they think that the department is too busy to spare the time for process improvements. One interim step that can reduce workloads is automating steps in the closing process. Our research finds that a large majority (71%) of companies that use automation substantially in the close are able to complete the process within six business days, compared to 43 percent that use some automation and just 23 percent that use little or none. Many finance professionals don’t realize that the operation of their ERP systems can be automated to eliminate or substantially reduce the time accountants now spend in performing the close. Automation can eliminate the need for human intervention to move the process forward – for example, by automatically closing a subledger, generating the necessary journal entries consistently and accurately, and then validating that all necessary steps have been completed properly. Automation software is designed to perform all these tasks in the background while alerting process owners of exceptions that must be resolved or approvals that must be given. Companies can program the process of extracting data from applications or tables and entering it into others. In our research half of midsize and larger companies said they must pull together information from two or three vendors’ systems to complete their close; 38 percent have to collect it from four or more. Today, such data management may require having an individual run a report, perform additional calculations, organize results from this data and enter information into the ERP system. Automation software can handle this full range of tasks faster and more reliably.

Still, technology has an important role in making process improvement feasible. A CFO and controller may be reluctant to embark on a major overhaul of their close because they think that the department is too busy to spare the time for process improvements. One interim step that can reduce workloads is automating steps in the closing process. Our research finds that a large majority (71%) of companies that use automation substantially in the close are able to complete the process within six business days, compared to 43 percent that use some automation and just 23 percent that use little or none. Many finance professionals don’t realize that the operation of their ERP systems can be automated to eliminate or substantially reduce the time accountants now spend in performing the close. Automation can eliminate the need for human intervention to move the process forward – for example, by automatically closing a subledger, generating the necessary journal entries consistently and accurately, and then validating that all necessary steps have been completed properly. Automation software is designed to perform all these tasks in the background while alerting process owners of exceptions that must be resolved or approvals that must be given. Companies can program the process of extracting data from applications or tables and entering it into others. In our research half of midsize and larger companies said they must pull together information from two or three vendors’ systems to complete their close; 38 percent have to collect it from four or more. Today, such data management may require having an individual run a report, perform additional calculations, organize results from this data and enter information into the ERP system. Automation software can handle this full range of tasks faster and more reliably.

In some cases a slow close may be the result of nonfinance functions taking longer than they might to complete necessary tasks such as taking inventory. The finance department may face resistance to speeding things up from those functional groups. This is a management issue more than anything else. “A fast close is everyone’s business” should be the attitude that senior executives apply in these situations.

Even when a corporation begins to shave time off its close, it cannot let up. Continuous improvement is necessary to keep those gains from slipping away. Our research shows that companies that have regular monthly or quarterly reviews of their close process to uncover issues also close sooner than those that do this annually.

While software, people and data issues all contribute to a slow close, it’s essential to examine the existing process to identify opportunities for improvement. This should be done before assessing software options because it enables those involved to spot issues caused by, for example, inappropriate use of desktop spreadsheets or issues in data availability or quality. When all the steps are compiled for analysis, it becomes much easier to eliminate redundant or unnecessary ones and achieve greater consistency in how all are performed. Having a detailed view of all the steps makes it easier to determine whether restaging processes or changing their frequency will lead to a faster process.

We believe that how quickly a company closes its books is a useful measure of the overall effectiveness of its finance organization. Our research shows that nearly identical companies (that is, they share the same size, industry, ownership structure, centralization of accounting and number of ERP systems, among other factors) can differ considerably in the length of their closing processes. The reasons most frequently centers on process management and software; adopting a continuous improvement approach to closing sooner and using software to support a faster, accurate process can make the difference. Methodically addressing process issues is essential to shortening the close, and it takes management focus to begin and sustain the effort. CFOs and controllers who are serious about making the finance function play a more strategic role in their corporation must make it a priority to complete the close within a business week.

Regards,

Robert Kugel – SVP Research

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).