At this year’s Global Pricing Forum, host Nomis Solutions announced the availability of its Discretion Manager software, which supports dynamic price negotiations. The annual event brings together thought leaders and practitioners interested in pricing. Nomis currently has 17 of the largest 100 banks as customers. With more customers, this year’s event had larger attendance than last year’s.

Discretion Manager helps loan agents set and adapt pricing terms and conditions to optimize the trade-off between loan volumes and margin, based on the preferences and characteristics of the lender. By dynamically recalculating the impact of changes on any number of terms being offered, agents are able to price more effectively. By tracking every negotiation, the system enables the agent’s company to capture competitive market intelligence and evolve its pricing tactics to respond to changing conditions. Discretion Manager can be accessed on a tablet, reflecting the vendor’s awareness of the need for mobility in situations such as automobile lending.

Nomis provides price and revenue optimization (PRO) software and services to financial services companies, including banks, automobile credit providers and credit card processors. Financial services is a distinct segment in PRO because customer attitudes and behavior with respect to money are distinct from those they have toward, say, travel and leisure or general merchandise. Especially for lending and insurance, adverse selection is a characteristic that should be incorporated into pricing models, but it rarely is. Riskier borrowers, for example, are more willing to pay higher interest rates so it’s important for the lender to ensure that pricing reflects the degree of principal risk it is undertaking.

Price optimization is based on a concept that is simple to describe but difficult to execute because even buyers with identical demographic characteristics (such as age, income or location) may have different degrees of price sensitivity. In the case of financial services, for example, those with low price sensitivity may place more value on other characteristics of a transaction. These may include service levels or service bundles, features (specific terms and conditions such as prepayment flexibility), convenience or brand values (including security, reliability or efficiency). By appropriately structuring its offers, a financial services company can get closer to its optimal trade-off between volume and risk-adjusted profitability. Nomis claims that it has been able to increase the net interest margins of its customers by five to 25 basis points (0.05% to 0.25%) over the course of a business or interest rate cycle; such an improvement has a meaningful impact on an institution’s return on equity. Margin improvement is partly the result of replacing top-down static pricing approaches (such as weekly or monthly price books sent out by headquarters) with a system that learns and recalibrates optimal terms even for multiple-variant offerings (such as size of down payment, initial and long-term interest rates and length of loan) based on real-time market feedback.

The development and growing sophistication of packaged PRO applications has been one of the most important advances in business analytics over the past decade. The potential benefits of such systems are widespread and evident. At its most basic level, PRO software allows companies to vary the price they offer according to an assessment of the price sensitivity of the individual buyer. Those assumed to be more sensitive are shown a lower price than those who are insensitive. Today’s products can accommodate differences in the context of offerings, especially variations on initial pricing and discount. For example, some customers prefer “everyday low prices” while others crave coupons and discounts. These are retail pricing approaches, but the same tactics apply to consumer banking and finance. In the end, the lender may receive exactly the same amount of revenue, but using the right pricing dynamics to attract a customer can make all the difference in getting the business. Nomis has been increasing its attention to managing the dynamics of the pricing discussion, which can be especially important for auto loans and other consumer finance products.

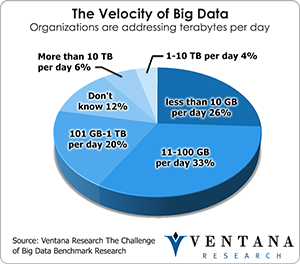

Optimization methodologies such as PRO are a natural fit for the application of big data analytics. Focus on this topic has increased in recent years because of the opportunity to gain ongoing actionable insights from the mass of data created by internal systems and publicly available data (such as social media). Our benchmark research shows that three-fourths of companies are addressing more than 10 gigabytes of data per day and 10 percent are already dealing with a terabyte or more. It requires sifting through large data sets to collect consumer behavior characteristics that will enable a company to identify customer segments and quantify their price sensitivity. These complex calculations require software designed for the purpose, but most in the financial services industry rely on older methods that produce less than optimal results. Big data analytics software can help organizations more closely manage the process of defining offers to customers (and the levels of discretion they allow to account managers and sales people) and the terms and conditions of the transaction.

application of big data analytics. Focus on this topic has increased in recent years because of the opportunity to gain ongoing actionable insights from the mass of data created by internal systems and publicly available data (such as social media). Our benchmark research shows that three-fourths of companies are addressing more than 10 gigabytes of data per day and 10 percent are already dealing with a terabyte or more. It requires sifting through large data sets to collect consumer behavior characteristics that will enable a company to identify customer segments and quantify their price sensitivity. These complex calculations require software designed for the purpose, but most in the financial services industry rely on older methods that produce less than optimal results. Big data analytics software can help organizations more closely manage the process of defining offers to customers (and the levels of discretion they allow to account managers and sales people) and the terms and conditions of the transaction.

The conceptual framework for PRO is well established. The challenge is in putting it into practice. For example, it’s not always easy to get reliable data about historical transactions, identify segments correctly and regularly update the data to reflect changes in markets, competitive moves and model refinements. There’s a change management aspect to PRO as well. Changing how an organization interacts with customers to take best advantage of technology can be challenging. For example, the best customers of a bank may be the least price sensitive, yet there’s a tendency to reward them excessively by offering better deals than they need to be satisfied. For that reason, sales incentive management and PRO are highly complementary. I’d say it’s impossible to get full benefit from either without combining them. Incentive management may be the only reliable means to overcome organizational inertia, especially where deep-seated beliefs are concerned.

It seems as if businesses have been struggling with pricing their products and services forever. At the dawn of the Internet age some pundits speculated that the increasing pricing transparency afforded by the Web would drive prices closer together. This hasn’t happened, and vendors are still challenged to set the best price. As well, for decades, financial services companies have been grappling with the difficulty of implementing customer value pricing as a way to deal with the extreme asymmetry of customer profitability in their industry. That is, a small minority of customers are very profitable while most are marginally profitable or even unprofitable. The dilemma facing executives that customer value pricing seeks to address is that some in the larger group can become very profitable if the institution can attract a higher share of their wallets or over time as their age, income and wealth grow. Without the right software it’s never easy to find such diamonds in the rough. Nomis can help financial services companies here, but although software is necessary, it’s not sufficient. Discussions with customers confirm the persistence of intractable cultural and institutional barriers that get in the way of successfully implementing a customer value approach.

Because of the host’s new software release, one area of focus of this year’s forum was managing discretion in setting prices. In many retail settings in western societies, prices are not normally negotiated. However, for many big-ticket consumer items (such as cars and houses), buyers usually expect to negotiate the price with the seller. In these cases, companies need to decide to what degree to give their agents discretion to negotiate charges, terms and conditions. There’s a high degree of dissatisfaction among business executives with how to apply discretion to the negotiation process to optimize revenues and profits; many suspect that too much discretion erodes margins. One reason for this distrust is poor application of incentive management to the process. Much of it, though, stems from a failure to understand buyers’ price elasticity and the optimal method of presenting prices in terms of list and discount in managing a negotiation. As noted, even for the identical product offered by the same company, for some customers it’s better to quote a high list price and offer a sizable discount while for others a more moderate list price and a limited discount works best. Nomis can help manage the dynamics of the price presented and discounts offered in a way that optimizes revenue and pricing.

Price and revenue optimization is only beginning to mature in industries other than travel and hospitality. While some financial services companies run their own internal PRO efforts, most don’t have the resources, desire or ability to do this in-house. Yet there is evidence of the value of PRO as an effective profitability management tool in the financial services industry. The need for banks and other financial institutions to increase their returns on assets and therefore equity in today’s challenging and more regulated environment makes PRO a vital tool. Financial services firms should take steps to incorporate more effective pricing as part of their strategy and consider Nomis Solutions to provide the analytical and operational underpinnings of such an effort.

Regards,

Robert Kugel

SVP Research

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).