New rules governing revenue recognition for contracts have gone into effect for larger companies and are about to go into effect for smaller ones. The Financial Accounting Standards Board (FASB), which administers Generally Accepted Accounting Principles in the U.S. (US-GAAP), has issued ASC 606 and the International Accounting Standards Board (IASB), which administers International Financial Reporting Standards (IFRS) used in most other countries, has issued IFRS 15. The two standards are very similar and will require fundamental changes in revenue recognition for companies that use even moderately complex contracts in their dealings with customers. These include, for example, contracts that are structured using tiered pricing or volume discounts or ones that routinely involve modifications, such as subscriptions that add or drop users and services or allow seasonal changes or promotional discounts.

The change in how revenue is recognized is challenging not only accounting staffs. Financial planning and analysis (FP&A) organizations in finance departments must adapt to the new standards as well. Those affected will need to be able to plan “events” – for example, closing a sale or paying commissions – and the accounting for those events in parallel. The timing of these events can be materially different from their recognition for accounting purposes. This disparity will give rise to the question: Is the variance we see in the numbers timing- or event-driven? s Those that currently use desktop spreadsheets for planning and budgeting should consider adopting dedicated planning and budgeting software to cope effectively with the increased complexity of planning in this new environment.

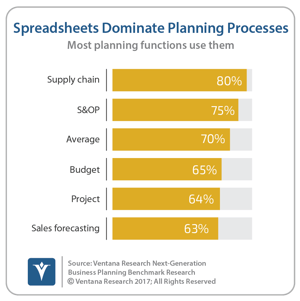

Companies affected by the new standards must assess their planning and budgeting processes to be sure they have the appropriate systems, processes and training to handle the more complex issues that arise from the new standards. Spreadsheets aren’t the right tool for this purpose. Timing variances between events and revenue recognition are both period-specific and cumulative. This is because the “events” are period-specific while revenue recognition for these events can occur over multiple accounting periods. Anyone who has grappled with modeling and measuring variances for similar types of differences will understand why using spreadsheets is arduous and error-prone and therefore not a practical choice. Yet our Next-Generation Business Planning benchmark research finds that two-thirds (65%) of companies use spreadsheets to manage their budget process. A dedicated planning application enables these  organizations to use actual data rather than opinion to understand whether a difference was due to the new accounting rules or poor performance. To be able to accurately measure performance, FP&A organizations need to track both events and revenue recognition in parallel.

organizations to use actual data rather than opinion to understand whether a difference was due to the new accounting rules or poor performance. To be able to accurately measure performance, FP&A organizations need to track both events and revenue recognition in parallel.

With the new accounting standards, the lag between when an event occurs – such when a contract is signed – and when a company recognizes revenue and expense from it may be more variable and less predictable than has been the case in the past. In extreme cases, performance measured by financial accounting will diverge materially from the “real” economic performance of the organization. Consequently, executives, especially those leading publicly listed companies, will need the ability to look at their results versus plan from both perspectives and distinguish between the event- and accounting-related variances in assessing and communicating their company’s performance.

In companies where the timing of revenue recognition can diverge substantially from current methods, FP&A groups will need to be able plan using models that incorporate financial and managerial accounting methods in parallel. They will need to be able to identify actual-to-plan variances caused by differences in contract values booked in a period and differences between the expected and actual timing of revenue recognized from contracts signed in a period.

A significant number of organizations – either entire corporations or business units with revenue responsibility – will need to change their approaches to creating and using planning models. Businesses that have large, complex contracts with their customers, such as those in the aerospace, construction and engineering industries, are likely to find that they need to plan and track results by contract – at the very least the 20 percent of their contracts that account for 80 percent of their revenues.

Another type of company or business unit that will need to adopt a more granular approach to tracking contracts under the new rules is one in which there are significant differences between the timing of revenue recognition for different types of contracts. Even if the value of individual contracts booked in a period is an insignificant percentage of the total, it may be necessary for organizations to segment contract bookings and revenue recognized for each major type of contract. This would be the case if there are significant differences in the timing of revenue between types of contracts or the mix of contract types varies from one month to the next.

Of course, not every company will need to change how it plans and budgets, such as those that are in a cash business or that only use contracts that take six months or less to fulfill. Moreover, tracking individual contracts will be impractical for organizations if the number of transactions makes it is too expensive and time-consuming to capture the relevant terms and conditions for each contract, which is necessary to be able to isolate the factors driving actual-to-forecast or budget variances. Under these circumstances the challenge for FP&A groups will be creating models that accurately forecast the average lag between contract signing and when revenue is recognized.

Even companies with longer-duration contracts don’t have to adapt if individual contracts account for an insignificant percentage of revenue. However, there’s one exception: if the contracts have significantly different revenue recognition profiles and the mix of those types of deals varies significantly between periods. For example, say that with one of those contract types, which accounts for one-quarter of annual bookings, there is a consistent one-month interval between when the contract is signed and when revenue is recognized. But a second type of contract (representing 40 percent of annual bookings) can take up to several months before revenue can be recognized, and then it happens all at once. The remaining contracts are recognized during the 12 months after a contract is signed. Any significant differences in the mix of contract types signed from month to month will make it difficult to reconcile variances and accurately distinguish differences caused by better-than-expected or inadequate contract bookings from those caused by timing differences. So it’s necessary for these organizations to create and use models that segment revenue by mix of contract types.

Companies that are experiencing a significant change in the timing of how they recognize revenue under the new accounting standards must determine whether it will be necessary to plan and budget for “real” and accounting data in parallel. If so, and if their company currently plans and budgets using desktop spreadsheets, I strongly recommend that they look into acquiring a dedicated planning application. In addition to dealing with increased complexity, this type of software can improve the budgeting and planning processes, making them more efficient.

Regards,

Robert Kugel

SVP & Research Director

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).