Pricing is an issue that almost every for-profit company confronts – and usually agonizes over. Organizations’ approach to pricing can range from centralized to decentralized and from highly disciplined to lax. Whether pricing is best handled in a centralized or decentralized fashion depends a great deal on the markets the company is serving as well as its organizational structure and culture. However specific pricing policies are established, though, a disciplined approach to price setting and negotiation is always superior to an ad-hoc process. Discipline is key to preventing margin “leakage” caused by unnecessary price concessions. Configure, price and quote (CPQ) software is a critical component in any leakage-prevention strategy.

In some countries, operating profit margins are at historical highs despite companies having a limited ability to raise prices. Since emerging from the last recession, corporations have successfully held down costs as their businesses have grown. The average operating profit margin for the S&P 500 (a broad index of publicly-traded companies traded in the U.S. markets) has grown from 23 percent in 2008 to 46 percent in 2016. Since then, margins have been slipping, impacted by rising costs and a still-limited degree of pricing power in markets.

While zero-based budgeting and other cost-containment tactics are often used, they aren’t the only answer to sustaining profitability. In particular, preventing margin leakage through greater pricing discipline is today likely the most effective way for companies to add to their bottom line and prevent profit erosion. In my view, every CFO should take an active role in ensuring that his or her company has effective pricing methods and processes. Specifically, the CFO should understand how CPQ software can bake in a more consistently disciplined approach to pricing in negotiating sales.

CPQ software has been around for decades but has mainly been purchased by the sales and sales operations groups with limited involvement of the CFO. That’s because its original purpose was to quickly configure complex products to speed the sales process. The pricing element has only recently increased in importance. (More on this below.)

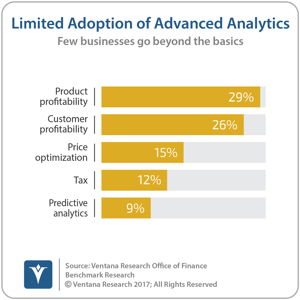

Moreover, pricing isn’t really the domain of the CFO. As a rule, finance departments shouldn’t determine prices because they lack front-line engagement with markets and customers. However, because he or she is responsible for fiscal control, the CFO should be heavily involved in ensuring that the company is using a disciplined approach to pricing. Despite this, our Office of Finance research finds that relatively few finance organizations have any role in managing profitability beyond cost containment. Fewer than one-third measure product profitability (29%) or customer profitability (26%). Only 15 percent have applied analytics to assist in price optimization.

Like almost all business issues, improving pricing discipline requires addressing an interrelated set of people, process, information (data) and technology (mainly software) conditions. The people issues center chiefly on roles, responsibilities, communications and compensation issues. The process issues revolve around establishing successful and repeatable processes for managing pricing – in other words, optimizing who does what and when.

To deal with these people and process issues, some companies have a dedicated pricing organization. In some cases, these groups are tactical in their approach to pricing: managing the creation of price lists, allowable discounts and other necessary elements of implementing pricing and pricing policy. Other pricing departments are more strategic. Their members understand pricing theory and how to apply it to their company’s circumstances and specific pricing processes and systems to better achieve the company’s strategic objectives.

As important and complex as the people and process issues can be, my focus here is on some of the software issues, especially as they relate to B2B businesses that mainly use a direct sales model.

A central piece of pricing management software is software that performs configure, price and quote functions. CPQ software, which was first introduced as packaged software in the 1990s, was originally created to simplify and therefore accelerate the process of assembling an accurate price quote for sales involving a complicated set of components. For example, buyers of large commercial trucks typically can choose from multiple engines, cab designs, transmissions and trailer types. Getting a quote back to a buyer quickly can be a competitive advantage since it improves a seller’s odds of securing the contract.

While the configure part of the process is still important, CPQ software has started to be used to manage revenue and margins. To minimize margin leakage, it can be used to control the discount from list price offered to the prospect on each component of the sale. The software also can give sales managers and representatives flexibility to apply their judgment to specific situations. For example, reps might be allocated a set amount of pricing discounts during a period and allowed to apply them as they wish.

The software also enables companies to modulate the degree of pricing flexibility according to the product (to move inventory or meet market share goals), region (based on quota attainment in the period to date), customer, or time of month or quarter (to achieve sales volume objectives). CPQ software can provide a built-in incentive to salespeople to maximize profitability by not requiring approvals for sales involving limited discounts. For example, to speed the process and increase their odds of closing a sale sooner, sales representatives will usually offer a 5 percent discount to customers initially if the sale is pre-approved rather than going for a maximum discount of 10 percent that must go through a deal desk for an OK.

The configure element also can contribute to margin because, on the other side of the sale, purchasing departments often are evaluated on the discounts they secure in their negotiations. They may therefore be highly sensitive to the pricing and discount offered on the core item of an order but less sensitive to shipping and handling costs or the price of complementary goods or services that are part of a contract bundle. Some CPQ software prompts salespeople to recommend highly profitable complementary products and services to the buyer to increase the size of the transaction and boost margins.

While controlling costs is a traditional responsibility of the CFO, that alone is no longer enough. He or she must step up to a leadership role, supporting more effective pricing strategies and practices. Leadership by the CFO is necessary because of the change-management aspects of adopting a new approach to pricing and because of the impact that a new approach to pricing can have on the company’s profitability and financial position.

For their part, finance departments should be more involved in pricing and profitability analytics. At the very least, they should be able to provide analyses of the impacts of variances in volume and pricing on results – especially in identifying the sources of margin leakage and its impact.

Regards,

Robert Kugel

Senior Vice President Research

Follow me on Twitter @rdkugelVR

and connect with me on LinkedIn. www.linkedin.com/in/robertkugel

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).