These days it strikes me that the motto of successful salespeople – "ABC: Always Be Closing!" – should apply equally to corporate controllers, albeit in the accounting sense. This is a reference to an approach to managing the finance department that I have been advocating, which I call "continuous accounting." It is a holistic way of managing the accounting function that, in large part, emphasizes using technology to distribute workloads more evenly over an accounting period, spreading closing activities as evenly as possible over time rather than waiting until the end of the month or quarter. Continuous accounting also stresses improving staff efficiency by automating repetitive processes as well as enhancing organizational effectiveness by improving data integrity in finance processes.

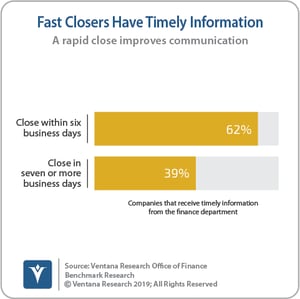

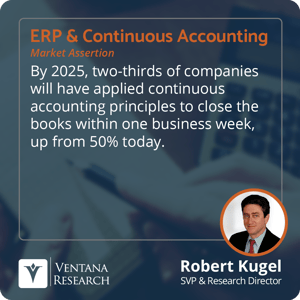

By consensus, organizations should close their books within one business week, yet our Office of Finance Benchmark Research finds that only one-half of them are able to meet that goal in their quarterly close. This is not a trivial matter – there are solid business reasons for closing within a week. An important one is that a fast close enables company executives and managers to access essential performance metrics quickly and take action sooner to address an opportunity or issue. Our research confirms this correlation: 62% of companies that close their books within six business days said they have timely information available to run the company, compared to just 39% of those that take more than two business weeks to complete the process. In part because of the investments that organizations have made in technology over the past year to be able to operate remotely, we assert that by 2025, two-thirds of companies will be able to meet that goal.

By consensus, organizations should close their books within one business week, yet our Office of Finance Benchmark Research finds that only one-half of them are able to meet that goal in their quarterly close. This is not a trivial matter – there are solid business reasons for closing within a week. An important one is that a fast close enables company executives and managers to access essential performance metrics quickly and take action sooner to address an opportunity or issue. Our research confirms this correlation: 62% of companies that close their books within six business days said they have timely information available to run the company, compared to just 39% of those that take more than two business weeks to complete the process. In part because of the investments that organizations have made in technology over the past year to be able to operate remotely, we assert that by 2025, two-thirds of companies will be able to meet that goal.

Our research has consistently found that, contrary to what one might assume, the time it takes a company to complete its close is unrelated to the size of the organization, its industry, or the number of ERP systems it uses. Using ineffective technology certainly plays a role in prolonging the close, and poorly designed or badly executed processes also prolong the close. Conversely, a well-designed, well-executed process that uses the right technology opens an avenue to accelerating a company’s close.

Closing the books is a highly definable, repetitive procedure, similar in that way to a manufacturing process. In both cases, attention must be paid to the design of the process and how well it is managed. The close must be examined step by step to determine, for example, whether there are unnecessary or redundant steps and whether the steps are in the most efficient sequence. The execution of the process must be evaluated to confirm that handoffs between individuals are always crisp and that exceptions are handled quickly. As in manufacturing, it is important to take a total quality management approach – one in which design of the process and related methods eliminates as many sources of defects as possible. For that reason, it is important to avoid using spreadsheets as much as possible because they are an unavoidable source of errors. Building quality into the process minimizes the need to spend time discovering the source of a mistake and then fixing it.

Closing the books is a highly definable, repetitive procedure, similar in that way to a manufacturing process. In both cases, attention must be paid to the design of the process and how well it is managed. The close must be examined step by step to determine, for example, whether there are unnecessary or redundant steps and whether the steps are in the most efficient sequence. The execution of the process must be evaluated to confirm that handoffs between individuals are always crisp and that exceptions are handled quickly. As in manufacturing, it is important to take a total quality management approach – one in which design of the process and related methods eliminates as many sources of defects as possible. For that reason, it is important to avoid using spreadsheets as much as possible because they are an unavoidable source of errors. Building quality into the process minimizes the need to spend time discovering the source of a mistake and then fixing it.

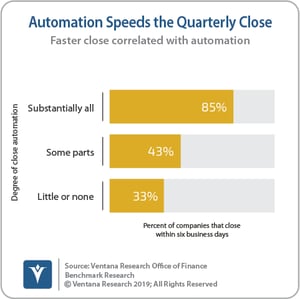

Our fast-close research leads us to conclude that having overly manual processes is a major reason why the average time to close increased over the past decade. Our research also finds a correlation between the degree to which companies have automated their close and how soon they are able to complete the process: 85% of companies that have substantially automated their close said they close their books within six business days, compared to only 43% of those that have automated some of their close processes and just 33% of the companies that apply little or no automation.

Technology – or rather the lack of it – explains the classic accounting calendar, but it is so ingrained that almost nobody even thinks about it. Much of what we think of as "normal" bookkeeping and accounting procedures are actually rooted in the centuries-old limits imposed by paper-based systems and manual calculations. Periodic processes that are performed, say, monthly or quarterly, developed as the best approach to organizing, coordinating and executing the calculations needed to sum up the debits and credits in journals and ledgers. The pacing of these manual systems represents a trade-off to balance efficiency against control. Their timing is the result of having to wait for there to be a sufficient volume of entries to justify taking accountants offline to perform manual summations, adjustments and consolidations. At the same time, companies need to maintain financial control by regularly checking their books for fraud, procedural issues and errors. In practice, weekly was generally too short a period to be efficient, while quarterly was too long to maintain control. That is why there are so many monthly tasks.

Technology – or rather the lack of it – explains the classic accounting calendar, but it is so ingrained that almost nobody even thinks about it. Much of what we think of as "normal" bookkeeping and accounting procedures are actually rooted in the centuries-old limits imposed by paper-based systems and manual calculations. Periodic processes that are performed, say, monthly or quarterly, developed as the best approach to organizing, coordinating and executing the calculations needed to sum up the debits and credits in journals and ledgers. The pacing of these manual systems represents a trade-off to balance efficiency against control. Their timing is the result of having to wait for there to be a sufficient volume of entries to justify taking accountants offline to perform manual summations, adjustments and consolidations. At the same time, companies need to maintain financial control by regularly checking their books for fraud, procedural issues and errors. In practice, weekly was generally too short a period to be efficient, while quarterly was too long to maintain control. That is why there are so many monthly tasks.

Even when computers began to automate the debits and credits, the old accounting calendars persisted. That is because the limits of technology forced software companies to use batch processing that could run only on weekly and monthly schedules. However, information technology has now reached a threshold to support transformation of core finance and accounting processes by enabling a continuous approach to transaction processing. Technology allows companies much more freedom to schedule their accounting-cycle tasks to distribute workloads across the period. For example, it is not necessary to do all intercompany reconciliations and eliminations at the end of the month – it can be done more frequently, reducing the end-of-period workloads, shortening the close, reducing the need for temporary staff and destressing the department. Technology, especially as it affects ERP and financial management systems, can also spread workloads more evenly. For instance, in many cases it is possible for corporations to cross-post intracompany transactions to eliminate discrepancies at their source. Increasingly, ERP vendors are adding analytic capabilities to these transactional systems to enable a weekly (or theoretically even a daily) soft close. That can substantially reduce the amount of period’s-end work that accounting departments must perform.

Accounting is a discipline that requires doing things exactly the same way over and over; that provides the necessary consistency. But doing it the same way is not necessarily the best way, which is why our definition of continuous accounting includes an emphasis on continuous improvement. “Always be closing” not only suggests spreading workloads more evenly, it also means continually examining the close process - the technology supporting it and human factors - for opportunities to shorten it and reduce the time and effort needed for its completion. Controllers who are committed to enabling their finance organization to play a more strategic role in their company should always be closing. With a determined effort, they can reap the benefits of doing so.

Regards,

Robert Kugel

Authors:

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for Ventana Research, now part of ISG. His team covers technology and applications spanning front- and back-office enterprise functions, and he personally runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).